The Maritime Vector

Bridging the gap between the world's largest industries and the global innovation economy

The Maritime Vector

A Familiar Pattern

In 1999, Jack Ma identified a structural gap hiding in plain sight.

Millions of Chinese factories could manufacture at enormous scale — textiles, electronics, consumer goods, components. Millions of buyers around the world needed what they made. Neither side could easily find the other. The factories didn't speak global commerce language. The buyers rarely navigated Chinese trade channels. The brokers who connected them — mainly Hong Kong trading houses — operated inside narrow networks that served a fraction of what the market could bear. Both sides had capacity. Both sides had demand. And between them — a structural void where connectivity should have been.

Ma didn't build a factory. He didn't become a buyer. He built the translation layer between them — making invisible nodes visible, turning specialised vocabulary into searchable categories, giving both sides a way to find each other.

The forces pushing Chinese manufacturing toward global markets were already strong — WTO accession was coming, global demand was real and rising — and they would have produced results regardless. What wasn't inevitable was the speed, the scale, or the form. Alibaba and the platforms that followed compressed what might have been decades of gradual convergence into years. By 2012, China had overtaken the United States as the world's largest e-commerce market, processing over $190 billion in online transactions. That outcome was not a given.

The same structural disconnection — same barriers, same void, same scale — exists today between the global innovation economy and the industries that run the physical world.

80% of the Real Economy, Nearly Invisible

The industries that move goods, generate energy, grow food, supply water, provide infrastructure, among others, represent roughly 80% of the real economy.

Their exposure to the global innovation economy is as low as 1-3%.

Not because the capabilities don't exist. Not because the capital isn't there. The technologies, innovations, proven applications, and business models that could transform these industries already exist — in other industries and domains, under other names. The nodes have not been connected.

Maritime: Underserved and "Underleveraged"

Among essential industries, maritime is one of the most prominent examples of what disconnection looks like at scale. A $2 trillion industry. The largest physical infrastructure on a surface that covers 7/10 of the planet. 90% of all physical goods pass through fewer than 55,000 nodes. Petabytes of data generated daily. Deep operational competence across tens of thousands of companies.

And yet the market values them only at the sum of their physical parts. Maritime companies, as example, trade at price-to-book ratios of 0.9-1.2x — against an S&P 500 average of roughly 4.5x. Across the S&P 500, intangible assets — tech, data, intellectual property, new business models — now represent over 90% of market value. In maritime, the inversion is near-total: roughly 10% intangible, 90% physical.

This is not a judgment on the industry's competence. It is the market pricing the absence of new products, services, and businesses that the innovation economy creates — and that the maritime industry has had almost no exposure to. The assets are there. The competence is there. What is missing is the connectivity that turns operational competence into innovation driven growth.

Two Sides of the Same Void

The industry. Tens of thousands of maritime companies operating a $2 trillion industry with deep operational competence, vast assets, and unmet needs they cannot address with what they can see. For them, connectivity to the innovation economy means access to solutions, capabilities, and business models that already exist — built and proven in other industries — but are invisible under the current structure.

The innovators. Millions of entrepreneurs, startups, scale-ups, and R&D institutions building solutions that are directly applicable to maritime challenges and opportunities — under different names, in different markets. For them, connectivity means access to a $2 trillion industry that could be twice the size.

Each side is barely aware of the other — and almost completely unaware of the potential the other represents.

The Missing Nodes

Even if both sides could see each other perfectly, very little would happen.

Fifty startups and twenty maritime companies in a room produce nothing. A registry of maritime companies shown to startups tells them nothing actionable. A database of startups shown to port operators is equally opaque. Both directories exist today. Neither generates connectivity at any meaningful scale.

The reason is structural: there are no intermediate nodes between the two sides. No well defined representations of where specific needs meet specific capabilities. No shared context that makes any given pair relevant to each other. What is missing are clearly defined spaces where industry assets, capabilities, and footprint can be leveraged to create new products and businesses — opportunity spaces. Without them, there is nothing to connect through. They are the prerequisite.

A Vast White Space

Maritime's structural position — the infrastructure layer through which 90% of physical goods flow — creates one of the largest untapped commercial landscapes globally. Thousands of concrete opportunity spaces where new products and businesses can be built from the industry's existing assets, capabilities, and footprint.

These stem from directly identifiable sources including:

Global forces that need the industry's structural position. Supply chain resilience, food and water security, energy transition, climate adaptation, trade provenance, among others — where maritime is irreplaceable and very little has been created (maritime is mentioned as a needed enabler in more than 90% of all UN SDGs).

Industry challenges that cost the world. Misdeclared hazardous cargo, slow and rigid operational structures that take months to adjust, untraceable commodities and source of origin, operational failure in key nodes that lead to global disruptions, food wasted in supply chains ($1T/year), among others.

Assets the industry holds but has never turned into products. Petabytes of sensor data generated daily, applied to nothing beyond optimising internal operations. The closest physical infrastructure humanity has to 70% of the planet's surface. A system through which physical goods spend often more than 50 days — during which almost nothing is done for the beneficial cargo owner beyond moving cargo from A to B. And much more.

Combined with:

A technology landscape where multiple inflection points have landed in the same window. Sensing, connectivity, compute, AI, biotech, energy storage — each on an exponential trajectory. The arena for creating new products and businesses from these opportunity spaces has never been larger. And yet the vast majority of industry leaders are focused on how these technologies can reduce their operational footprint only. Almost none are asking how they can expand it.

Lost in Translation

Even with opportunity spaces defined, three forces prevent connection — and they reinforce each other.

Vocabulary. A port operator needing to optimise how vessels share berths will never find the scheduling software built for exactly that problem in another industry, because neither side uses the other's words. You cannot find what you cannot name in the other side's terms.

Visibility. The two sides exist in entirely separate information ecosystems — different events, publications, networks, procurement channels. They are not ignoring each other. They are invisible to each other.

Behaviour. Industries default to building internally because external search has never worked. Innovators default to markets they can already see. The absence of connection has become the default.

And two conditions are missing entirely.

Connectivity. Relevant nodes remain inert without a mechanism that turns proximity into interaction — structured pathways from identification to conversation to transaction.

Density. Network effects require concentration. Unqualified participants in a room produce nothing. The same group, concentrated around a specific opportunity space, have a meaningful probability of results.

Without the missing nodes, there is nothing to connect through. Without overcoming the barriers, neither side finds them. Without density and connectivity, even well-placed nodes produce nothing. All five reinforce each other. Together, they produce near-total isolation.

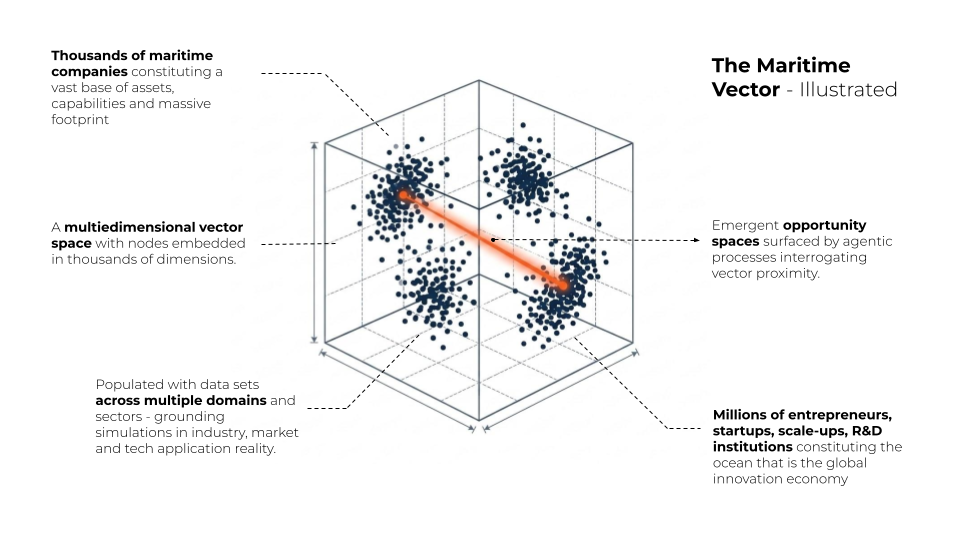

The Vector

What Alibaba built for commerce between China and the world, someone needs to build for innovation between the global innovation economy and the industries that run the physical world.

We call it Maritime Twin.

A continuously operating and agentic intelligence engine that maps the maritime industry's DNA against the global innovation universe — generating thousands of opportunity spaces that lead to tens of thousands of new product, business, and venture opportunities.

To achieve this, during 2026 Maritime Twin is mapping 48 sub-segments of the maritime industry — 15,000-25,000 companies, their assets, operations, market dynamics, and structural position — and matching them against 50,000+ startups, scale-ups, and solution providers found across all industries, drawn from a screening universe of roughly 1,000,000 companies, plus frontier R&D and pre-commercial science.

We are already working with industry corporations, entrepreneurs, and institutions to actualize opportunity spaces as they emerge. If you see what we see — and want to be part of building it — we welcome you to reach out and collaborate.

Maritime is one of the most prominent examples of this disconnection — and one of the largest opportunities. But the architecture is not maritime-specific. The same structural disconnection, the same five conditions, the same void exists in energy, water, food systems, infrastructure and every other essential industry. Each sector twin is designed to inherit the methodology, the tooling, and the compounding intelligence the engines before it have built.

The factories existed. The buyers existed. What Ma built was the layer between them. The industries exist. The innovators exist. What has been missing is the vector — the twin.

We are building it.